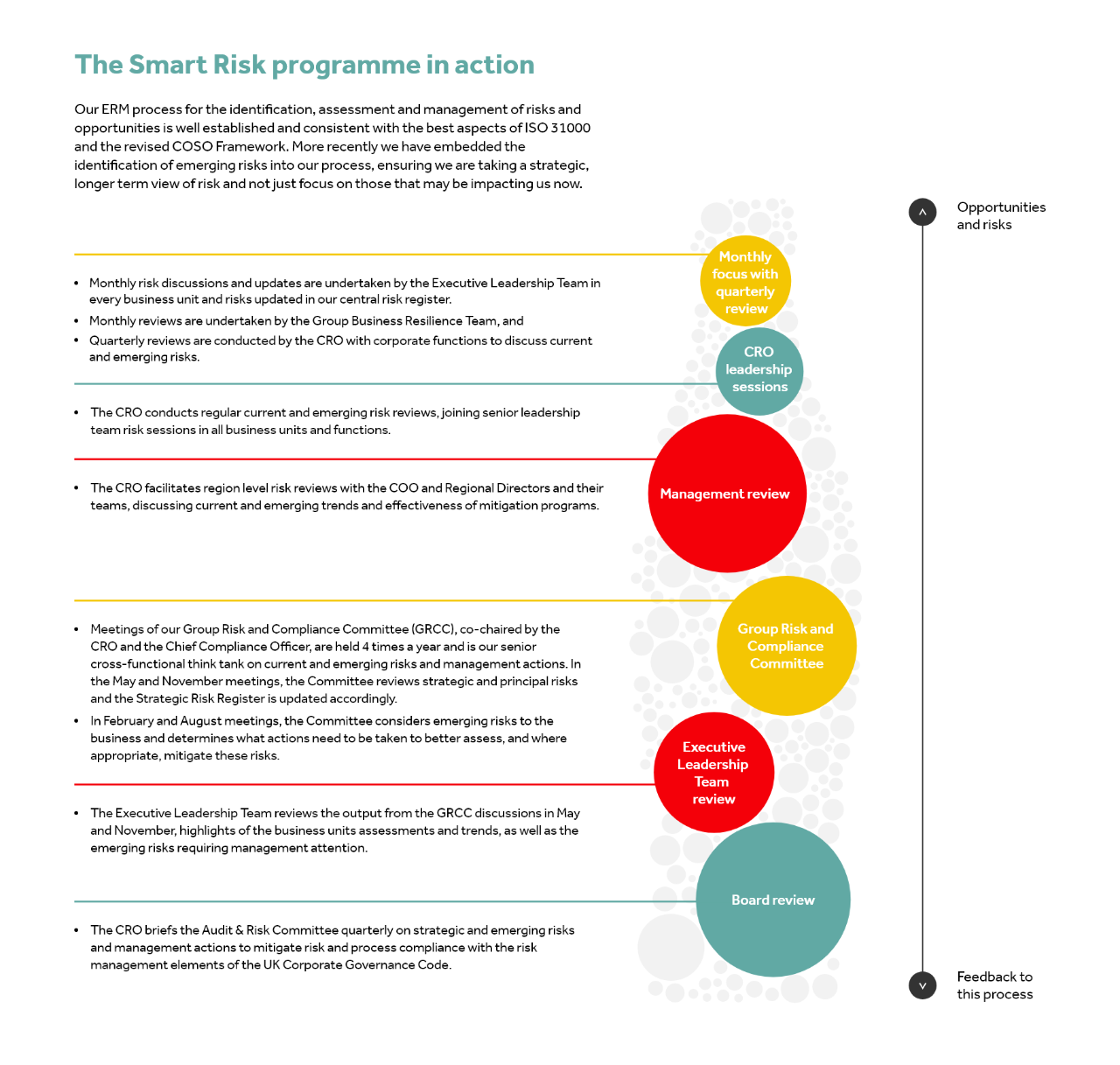

Overview of Emerging Risks

We are constantly reviewing changes in our operating environment and looking for trends that may have a longer-term impact on our business. As a result, our emerging risks can and do change regularly as we gather more information and review their potential impact.

For reporting purposes, we revise our Emerging Risks biannually and report key emerging risks on our website and Integrated Annual Report annually.

Our key emerging risks as at May 2023 are:

1. Development of Artificial Intelligence

Description of the risk

The application of artificial intelligence (AI) spans across several business processes and will support our acceleration of digital commerce and processes such as the automation of some of our beverage production, supplier ordering and customer fulfilment processes for example.

However, AI technology also poses various risks to our business due to a potential over reliance on the outputs of AI generated information, potential misuse by malicious actors and the potential of unintended consequences given many aspects of AI are not well known and there is little regulatory controls over its use.

We expect a number of business functions to start adopting some aspects of AI within their business processes in the near future. We expect AI to continue to advance and become increasingly complex and autonomous, presenting both risks and opportunities for our business.

Potential Impact

· Errors in the algorithms and/or biased AI data (intentionally or unintentionally) could lead to faulty planning decisions during our S&OP process leading to either over production and subsequent additional warehousing costs or additional waste (including food waste); or under-production leading to an inability to supply our customers with beverage products.

· Our use of AI could increase the “attack surface” available to malicious actors. Coupled with an enhanced ability of those actors to leverage AI to conduct attacks could lead to an increased risk of loss of proprietary or personal data and potential violations of rights to privacy of Coca-Cola HBC employees or customers and fines or regulatory actions resulting from non-compliance with privacy requirements, especially in our markets where the regulations are stricter.

· Our supply ordering, production, distribution, and financial systems are heavily dependent on information technology. The leverage of AI by malicious actors in cyber-attacks could increase the severity of interruption to our systems reducing our ability to supply our customers with beverage products.

Mitigating the risk

· We will establish a robust governance and operating model to ensure deployed AI technologies are secure, safe, ethical, and comply with internal corporate policies.

· We will establish a cross-functional team comprising of representatives from business functions, legal, IT, cyber and privacy teams to ensure compliance by design.

· We will establish and maintain a central inventory of all AI technologies that is mapped with specific business use cases.

· Our governance processes will ensure decision-making processes are lawful, transparent, explainable and there is clear accountability in AI technologies.

· We will take all appropriate actions to safeguard that personal data are collected, processed and used in a way that respects individuals’ privacy rights and freedoms.

· We will develop and communicate organisational policies on the acceptable use of AI technologies. Execute awareness campaigns to achieve long-term lasting behavioural changes.

2. The cost and availability of sustainable packaging

Description of the risk

Governments and non-government organisations are driving change through new regulations such as the EU Packaging and Packaging Waste Directive. We are not yet certain of what those regulations require of us.

We have publicly committed to a NetZeroby40 target however around 34% of our carbon emissions are generated by our use of packaging which means the packaging we use for our beverages in the future has a significant influence on our ability to meet our commitments.

In addition, major changes to our packaging require significant investments in new production lines and potential for redundancy in existing production lines and assets. It may require significant changes to our distribution systems and investments for our customers.

We have also identified a number of variables that, because of their longer-term nature, we don’t yet fully understand including the impact of significantly increased carbon prices flowing through to the price of PET, glass, and Aluminium.

Potential Impact

· Decreased availability and increased costs of packaging materials as a result of increased carbon pricing or additional taxes on packaging materials such as new PET, recycled PET, glass and Aluminium that are currently a critical part of our business strategy.

· The significant costs including capital expenditure, required in making major changes to our beverage production lines, including the purchase and installation of new lines and in redundancy of existing production equipment, to cater for different packaging.

· Impact on our customers and their business: e.g., introducing more refillable packaging materials would increase the amount of collection, storage, and reverse logistics.

· The impact on our reputation, and ultimately sales of beverage products, if we are not able to deliver our products in packaging that is acceptable to consumers at a price they are willing to pay.

· Potential opportunities for our business in leading the delivery of beverages in innovative, sustainable packaging.

Mitigating the risk

· In 2022, we continued to work on the development of a profitable packaging strategy that reduces our environmental impact and addresses escalating stakeholder concerns relating to packaging waste.

· In 2023, we expect to deliver our pack mix of the future project, including a comprehensive quantitative assessment of the risks and the financial impact in both operating expenses and capital expenditure associated with the various options including packageless and refillable SKUs. This will provide key long-term insights into our future packaging strategy and potential changes to our operating model that may be required over time, while remaining flexible enough to respond to changes over time.

3. ESG Risks in our Supply Chain

Description of the Risk

There is an increasing demand for transparency in environmental, social and governance (ESG) performance as the potential impact of climate change becomes clearer and companies are increasingly held accountable to contribute to reducing the drivers of climate change.

The EU Corporate Sustainability Due Diligence Directive will go the EU Parliament and Commission and if adopted, it is expected that EU countries will transpose the Directive into national law over the next two years that we will need to comply with. There are rightly expectations that companies identify and take action to ensure human rights, including appropriate working conditions and living wages, are respected, and implemented throughout their value chains. We may increasingly be held responsible for the actions or lack of compliance of suppliers deeper in our supply chain where we currently have less visibility. In addition, we are expected to use our influence in the value chain of which we are part to drive change.

Potential Impact

· We could be held responsible for suppliers involved in incidents of non-compliance which can lead to reputation risks, and fines as well as additional costs in finding alternative suppliers.

· Additional due diligence requires additional management time and effort increasing our costs.

· We may also have difficulty accessing ingredients that are impacted by climate change or we may have to pay more for those ingredients.

· We may not meet our stated sustainability goals by 2025, and future sustainability goals as it relates to ingredient sourcing and climate change

Mitigating the risk

We are continuing to build our relationships with suppliers through initiatives such as our supplier sustainability forums as well as greater engagement to ensure more sustainable sourcing (e.g. training, joint initiatives, joint sustainable goal setting etc.). Our buyers were retrained during the year on the sustainability risk assessment tools available for supplier selection and governance. We continue to expand the use of the EcoVardis system to support our supplier ESG performance assessments for better, more objective supplier monitoring. This will increase our visibility deeper into our supply chain.

We are conducting deeper assessments into the potential impact of climate change on our suppliers and the implications for our business. We will continue working with our suppliers to support them in setting and delivering on their sustainability goals, including setting science-based carbon reduction targets.

4. Cost and Availability of Water

Description of the risk

Water is fundamental to our business. It makes up the largest percentage of our products and is a key part of our production processes. It is also critical for our suppliers of agricultural ingredients, and for the local communities in which we operate. Maintaining high quality, reliable watersheds is not just critical for our business but also for our relationship with our communities and suppliers.

Climate change is expected to have a significant impact on watersheds around the world. According to the latest report from the Intergovernmental Panel on Climate Change (IPCC), more than half the world’s population faces water scarcity for at least one month every year and this will increase in the future.

During 2022, we updated our assessment of the potential impact of climate change on our business under two different climate scenarios (RCP4.5 and RCP8.5), including the availability (physical risk) and cost (physical and transition risk) of water by 2030 and 2040.

Our assessment indicated that climate change is not currently having a significant impact on the availability and cost of water but is likely to do so by 2030 in the climate scenarios that we considered. This is a result of an increase in the level of water stress particularly in areas that we have already determined are in water-stressed areas, which we refer to as “water priority” plants or locations.

In addition, the management of water resources is a key concern for a range of our key stakeholders and ranks very high in our annual materiality assessment. We expect increasing attention to water security concerns driven by the outcomes of events such as the UN Water Conference and potential for increased reporting requirements and government and non-government organisation pressure to reduce water usage.

Potential Impact

- If water availability decreases due to climate change or significant water withdrawal from upstream users, it also will lead to disruption of the water supply to our operations and to communities in which we operate.

- If we use significant amounts of water from the local watershed, it may reduce the availability of water for local communities and damaging our reputation.

- We have assessed that climate change could increase our annual baseline water costs by up to 48% by 2030 and 39% by 2040.

- We need to spend an additional €95.6 million in capital expenditure between now and 2040 to meet our water needs and to replenish watersheds for local communities in water priority areas

- For our suppliers, the water risk could lead to decreased crop yield, disruption of their supply processes, issues with quality of ingredients, decreased income, while for us it would lead to increased cost of ingredients or production disruption due to ingredients or raw materials not being available in the quantity or quality we expect.

For more details on our water risk assessment, please see page 76 of our 2022 Integrated Annual Report (IAR).

Mitigating the risk

In 2022, we:

- continued to implement water usage reduction plans across our operations;

- implemented water stewardship programmes in water priority locations to mitigate shared water risks;

- updated source vulnerability assessments for all plants and enhanced our plans, including identification of additional capital expenditure required for enhancing infrastructure.

In 2023, we will:

- further implement innovations to reduce our water usage, particularly in water priority locations.

- complete the inclusion of water usage data for our Egyptian plants in our water risk assessment.

- implement additional community water projects to help secure water availability for local communities in an additional four locations.

5. The impact of extreme weather on our production and distribution

Description of the risk

It is generally accepted that global warming has made significant changes to weather patterns. That means that the world is experiencing more frequent and more severe incidents such droughts and storms.

We do not believe these changes have significantly impacted our business yet. We do have and have had for long periods of time, production facilities located close to water courses known to be susceptible to flooding. We have production facilities located in areas known as being at higher risk for droughts and wildfires.

Depending on the global response to climate change, our production facilities and distribution networks may be impacted by extreme weather and its effects in the future. As there are so many variables, it is very difficult to accurately assess how climate change may impact us.

Potential Impact

· We may have disruptions to our production or distribution which reduces our ability to supply our customers. This may impact our reputation as a reliable supplier and lead to financial losses if we do not have sufficient product to sell.

· Events such as extreme storms, flooding or wildfires may damage our production facilities or equipment leading to financial losses

· Insurers may increase insurance premiums to cover increased property loss or business interruption risks associated with more frequent or more severe weather events

Mitigating the risk

In 2022, we conducted a comprehensive assessment of the risks to our production and distribution as a result of climate change using multiple climate change scenarios. Our assessment was focused on climate scenarios RCP4.5 and RCP8.5 although we also considered RCP1.9 (Paris Ambition aimed at keeping global warming to 1.5 degrees or lower) and determined that it had no discernible impact.

We identified 16 plants that may be impacted by climate change primarily wildfires, flooding and intense precipitation. We are developing adaptation plans such as fire suppression and landscaping changes, flood mitigation works and stormwater upgrade systems. We estimate that the costs of these adaptation plans will amount to €29m over the next five years.

In 2023 we are enhancing our contingency planning across all plants but particularly those that may be impacted by climate change in order to better understand support needs in the event of disruptions to our production and distribution.

In addition, we estimate that if insurers were to apply an estimated increase of 30-40% in insurance premiums to production facilities that we have identified as being at higher risks as a result of climate change, we could see an increase in our insurance premiums of €1.5m annually. In order to mitigate the potential rise in insurance premiums, we will collaborate with our insurers to ensure they understand how we have assessed these risks and the adaptation plans we are developing to mitigate them.